Featured

Table of Contents

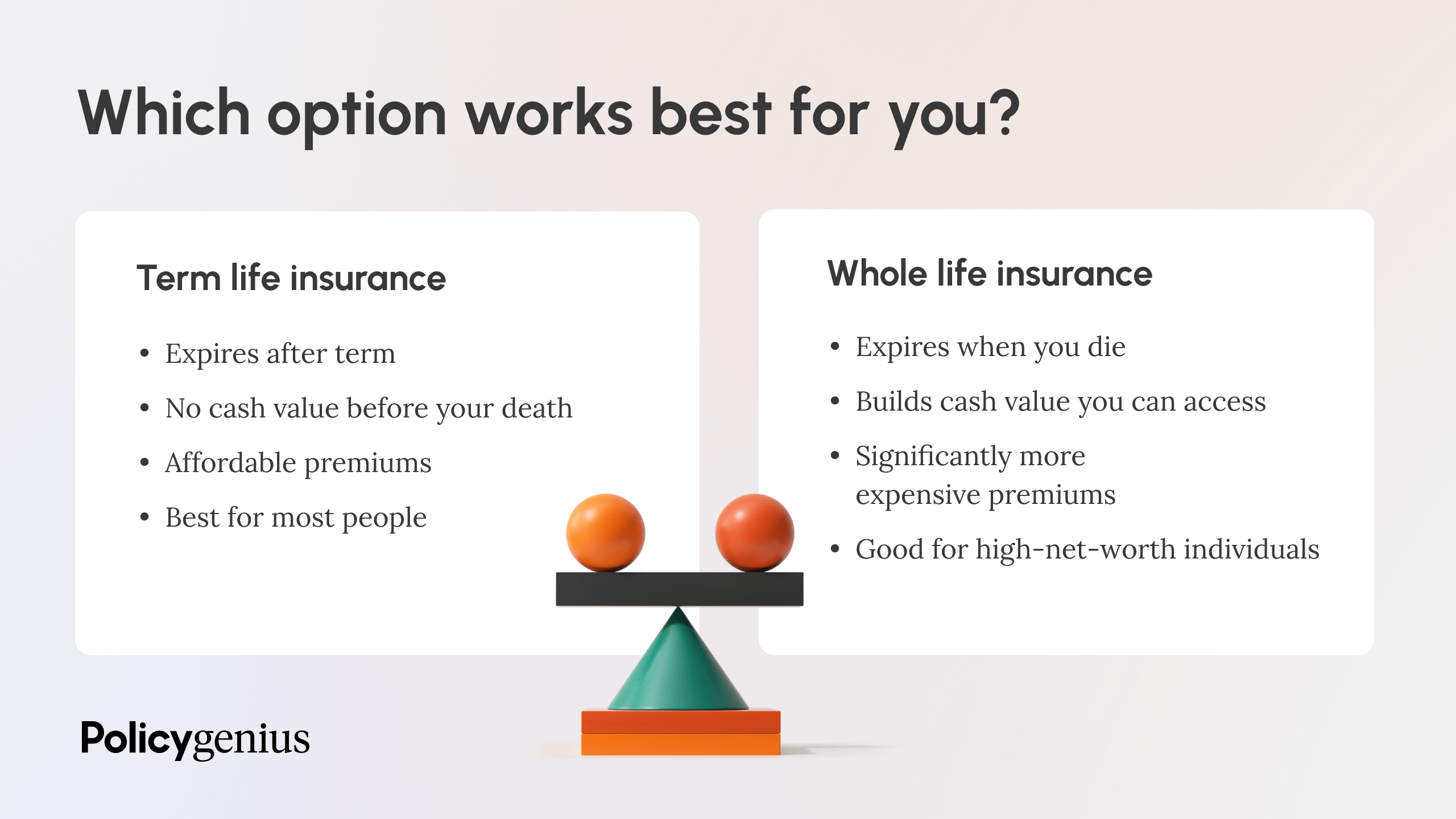

Degree term life insurance policy is just one of the most affordable coverage alternatives on the market due to the fact that it provides fundamental defense in the kind of fatality advantage and just lasts for a set period of time. At the end of the term, it ends. Entire life insurance policy, on the various other hand, is considerably extra costly than level term life since it does not end and features a cash value feature.

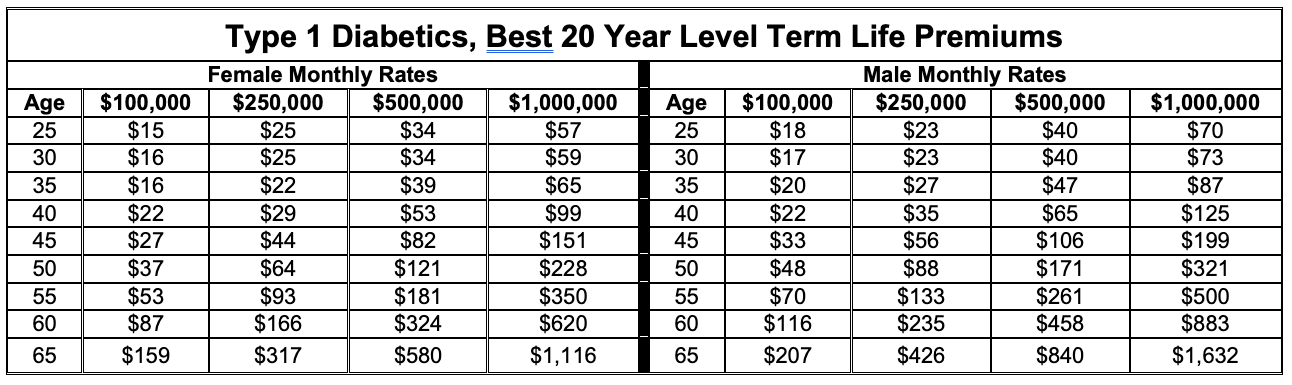

Prices might differ by insurance provider, term, insurance coverage quantity, health course, and state. Level term is a great life insurance option for most people, but depending on your coverage demands and individual scenario, it might not be the finest fit for you.

What is the most popular Level Term Life Insurance Vs Whole Life plan in 2024?

Annual eco-friendly term life insurance policy has a term of just one year and can be renewed each year. Annual renewable term life costs are initially less than level term life premiums, but prices go up each time you restore. This can be a good choice if you, for instance, have just stop smoking cigarettes and require to wait two or three years to look for a degree term plan and be eligible for a lower price.

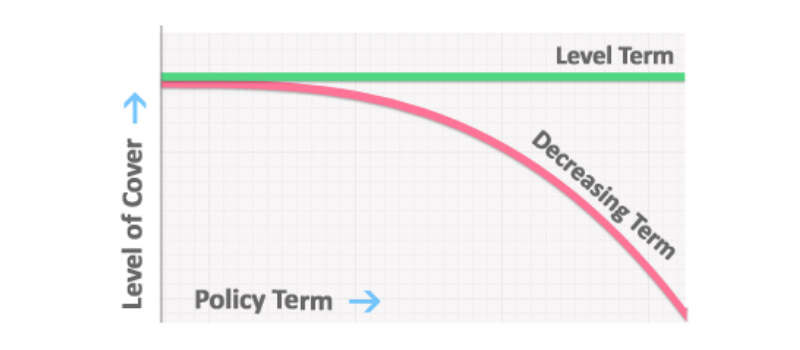

With a decreasing term life policy, your fatality benefit payout will certainly lower over time, however your repayments will certainly stay the exact same. Decreasing term life policies like home loan security insurance generally pay out to your lending institution, so if you're looking for a plan that will certainly pay out to your liked ones, this is not an excellent suitable for you.

Raising term life insurance policy policies can help you hedge versus rising cost of living or strategy economically for future children. On the other hand, you'll pay more upfront for less insurance coverage with a boosting term life policy than with a level term life plan. If you're unsure which sort of policy is best for you, functioning with an independent broker can aid.

How does Level Term Life Insurance For Young Adults work?

As soon as you have actually chosen that level term is best for you, the next step is to purchase your policy. Below's how to do it. Determine how much life insurance policy you require Your insurance coverage amount should offer your family members's long-lasting monetary requirements, consisting of the loss of your income in the occasion of your fatality, as well as financial obligations and daily costs.

As you search for methods to safeguard your economic future, you have actually most likely found a broad range of life insurance policy options. Selecting the ideal protection is a large decision. You wish to discover something that will certainly assist sustain your enjoyed ones or the causes essential to you if something happens to you.

Many individuals favor term life insurance policy for its simplicity and cost-effectiveness. Term insurance contracts are for a relatively brief, defined time period but have alternatives you can customize to your requirements. Certain advantage alternatives can make your costs change gradually. Degree term insurance policy, nevertheless, is a kind of term life insurance policy that has consistent settlements and a changeless.

Level Term Life Insurance Coverage

Level term life insurance policy is a part of It's called "level" since your costs and the advantage to be paid to your liked ones remain the exact same throughout the contract. You will not see any modifications in cost or be left asking yourself regarding its worth. Some agreements, such as every year eco-friendly term, may be structured with costs that enhance over time as the insured ages.

Fixed fatality benefit. This is also established at the beginning, so you can know exactly what fatality advantage amount your can anticipate when you pass away, as long as you're covered and up-to-date on costs.

How does Level Term Life Insurance Companies work?

You agree to a set costs and fatality advantage for the period of the term. If you pass away while covered, your death advantage will certainly be paid out to liked ones (as long as your premiums are up to date).

You might have the alternative to for an additional term or, most likely, renew it year to year. If your contract has an ensured renewability provision, you might not require to have a brand-new medical examination to maintain your insurance coverage going. Nonetheless, your premiums are most likely to boost since they'll be based upon your age at revival time. Affordable level term life insurance.

With this alternative, you can that will certainly last the remainder of your life. In this situation, once again, you may not need to have any type of new medical exams, but costs likely will increase as a result of your age and brand-new insurance coverage. Different companies supply numerous choices for conversion, make sure to understand your selections before taking this action.

Talking with an economic consultant additionally may aid you identify the course that aligns best with your general approach. Most term life insurance policy is level term throughout of the agreement period, yet not all. Some term insurance coverage may come with a costs that increases gradually. With lowering term life insurance policy, your survivor benefit goes down gradually (this kind is often obtained to especially cover a long-lasting financial debt you're settling).

Level Term Life Insurance For Young Adults

And if you're established for renewable term life, then your premium likely will go up yearly. If you're checking out term life insurance policy and intend to ensure straightforward and foreseeable monetary security for your family members, level term may be something to take into consideration. Nonetheless, as with any type of insurance coverage, it may have some limitations that do not fulfill your requirements.

Normally, term life insurance coverage is a lot more economical than permanent coverage, so it's a cost-efficient way to safeguard monetary security. Adaptability. At the end of your contract's term, you have numerous choices to proceed or relocate on from coverage, commonly without needing a medical examination. If your spending plan or protection requires adjustment, fatality advantages can be lowered in time and result in a lower costs.

Guaranteed Level Term Life Insurance

Similar to various other sort of term life insurance policy, as soon as the contract ends, you'll likely pay greater premiums for protection due to the fact that it will certainly recalculate at your present age and health. Repaired coverage. Level term uses predictability. However, if your financial situation adjustments, you may not have the required protection and might need to purchase extra insurance coverage.

But that doesn't mean it's a fit for every person. As you're looking for life insurance policy, right here are a couple of vital elements to take into consideration: Spending plan. One of the benefits of level term protection is you recognize the expense and the survivor benefit upfront, making it much easier to without fretting regarding rises with time.

Usually, with life insurance coverage, the healthier and more youthful you are, the a lot more economical the coverage. Your dependents and financial duty play a role in identifying your protection. If you have a young family members, for circumstances, level term can aid give monetary support during important years without paying for protection longer than essential.

{kind=link}

Latest Posts

Funeral Plans Compare The Market

Best Funeral Plan Company

Instant Life Insurance Quote Online